|

Update: On February 26, 2025, the European Commission published its first Omnibus package pushing for the simplification of existing sustainability reporting requirements. The changes outlined in the Omnibus are currently only a proposal and amendments could still be made during the EU legislative process. Companies that fell within the scope of the original Corporate Sustainability Reporting Directive (CSRD are encouraged to understand what the package entails and how it may impact their CSRD preparedness strategy. For further information on the proposed changes, refer to our Preparing for What’s Next: Navigating CSRD Amid Proposed EU Omnibus Changes blog post. |

The ESG reporting dam has broken. Officially. Which means business leaders are now swimming in an ocean of sustainability-related acronyms. Unfortunately, like boy bands, politicians, and infomercials, the acronyms can all start sounding the same after a while, including the first set of the European Sustainability Reporting Standards (ESRS).

So, to help you understand what these new standards could mean for your business, we're taking a closer look at the ESRS to help you game plan. Because, ready or not, the effective date for these landmark standards isn't too far down the road, so the time to start preparing is now.

Overview of the EU Corporate Sustainability Reporting Directive (CSRD) and ESRS

Since we recently spoke at length about the new CSRD from the European Union, we won't entirely repeat ourselves here. Still, we still want to briefly review the massive bowl of sustainability-related alphabet soup sitting in front of business leaders today, or at least what's happening at break-neck speed across the pond.

Like most regulators across the world, the European Commission (EC) recognized the need for a more standardized framework for sustainability reporting, knowing the Non-Financial Reporting Directive (NFRD) wouldn't cut the ESG mustard going forward. As such, the European Commission (EC) proposed the CSRD in April 2021, a sweeping set of regulations meant to promote transparent, comparable, and trusted sustainability reporting across companies with operations in the EU.

Fast forwarding a bit, the European Parliament and Council of the EU adopted the CSRD in November 2022 and, just a few months afterward, the regulations went into force on January 5, 2023. EU member states have 18 months from that January date to transpose the CSRD into law.

At the most basic level, the directive establishes a compliance baseline for EU member states, where they can add provisions during this 18-month period but can't eliminate any of the CSRD's requirements. Also, since the directive itself doesn't contain any actual sustainability reporting standards, the CSRD required that EC to adopt an initial set of standards, and that's where the ESRS enters the picture.

Drafted by the European Financial Reporting Advisory Group (EFRAG), the ESRS are a robust set of standards that spell out the reporting requirements for organizations falling within the reach of the CSRD. As a critical component of the EU's Green Deal agenda, these new standards are, in fact, as big of a deal as they sound and should not be taken lightly. So, on that note, let's roll up our sleeves and see what the ESRS have under the hood.

The Initial ESRS Package

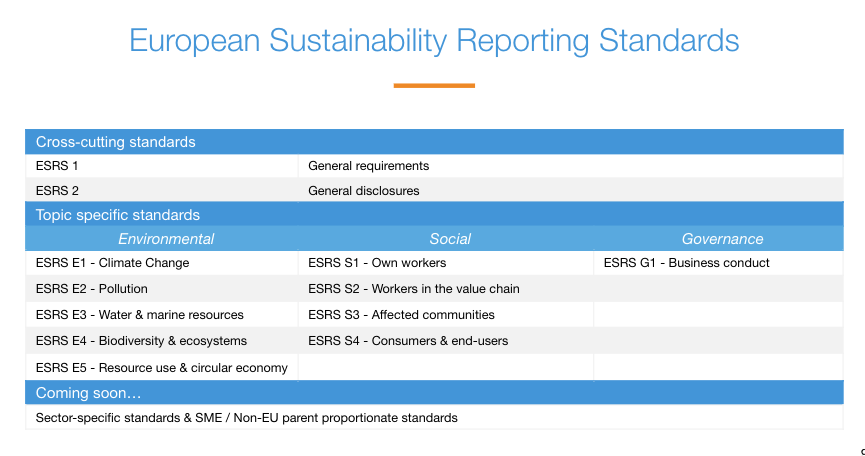

The first batch of ESRS consists of 12 sector-agnostic standards – two cross-cutting and 10 topical, categorized into environmental, social, and governance-related themes – that span the full range of sustainability matters within the CSRD. In total, the standards outline 84 disclosure requirements with over 1,100 quantitative and qualitative data points.

Two Cross-Cutting Standards

The ESRS package includes two overarching standards that apply to sustainability matters in general:

- ESRS 1 - General Requirements: This standard outlines the general principles and foundational requirements for sustainability reporting, ensuring consistency and comparability.

- ESRS 2 - General Disclosures: Focusing on strategy, governance, and materiality assessment processes, ESRS 2 enhances transparency and provides a comprehensive framework for reporting on sustainability-related impacts, risks, and opportunities.

Environmental Standards

The ESRS package encompasses a set of five environmental standards that shed light on various aspects of ecological sustainability. These standards facilitate reporting on the following key themes:

- ESRS E1 - Climate Change: This standard delves into the disclosure of climate-related impacts, risks, and opportunities, emphasizing the importance of addressing the challenges posed by climate change.

- ESRS E2 - Pollution: With a focus on reducing pollution and preserving the environment, this standard ensures that companies report on their efforts to mitigate the effects of pollution, both direct and indirect.

- ESRS E3 - Water and Marine Resources: Taking into account the critical importance of water and marine ecosystems, this standard guides companies in disclosing their sustainable practices related to such resources.

- ESRS E4 - Biodiversity and Ecosystems: Emphasizing the preservation of biodiversity and the sustainable management of ecosystems, this standard highlights the significance of responsible and thoughtful practices.

- ESRS E5 - Resource Use and Circular Economy: Addressing the efficient use of resources and the transition to a circular economy, this standard focuses on reducing waste and promoting sustainable practices throughout the value chain.

Social Standards

The ESRS package includes four standards dedicated to social sustainability, ensuring that companies report on their organizational practices in relation to social impact:

- ESRS S1 - Own Workforce: In this standard, companies disclose their commitments to their employees, including their approach to employee engagement, well-being, diversity and inclusion, and training and development.

- ESRS S2 - Workers in the Value Chain: Recognizing the importance of fair and ethical treatment of workers throughout the value chain, this standard ensures that companies report on labor rights, safe working conditions, and fair compensation.

- ESRS S3 - Affected Communities: Addressing the impact of business activities on local communities, this standard requires companies to report on their efforts to engage with and support these communities, ensuring responsible and sustainable practices.

- ESRS S4 - Consumers and End-users: Focusing on consumer rights, product safety, and responsible consumption, this standard highlights the significance of companies' efforts to meet consumer expectations and contribute to a more sustainable society.

Governance Standards

Understanding the importance of accountable and responsible governance, the ESRS package includes one standard dedicated to this aspect:

- ESRS G1 - Business Conduct: This standard emphasizes the significance of ethical and responsible business conduct, including the prevention of corruption and bribery, the promotion of transparency, and the recognition of human rights.

If the structure of the general, cross-cutting ESRS look familiar, that's not by accident. The EFRAG based the CSRD structure on the pillars of the Task Force on Climate-Related Financial Disclosures (TCFD) framework. Zooming in further on these two standards:

- ESRS 1 establishes key concepts and definitions, including value chain reporting, time horizons, and double materiality, all of which are foundational to CSRD-compliant sustainability reporting

- ESRS 2 includes required disclosures on the basis of preparation as well as the four pillars of governance – strategy, impact, risk and opportunity management (including the materiality assessment process), and metrics and targets

Also, take note that entities must comply with the general requirements of ESRS 1 and general disclosure requirements of ESRS 2, regardless of materiality. However, for the topical standards, companies must perform a materiality assessment to determine what is and isn't material to the enterprise.

Materiality Assessment Requirement

Speaking of materiality, this seems like the perfect time to discuss the materiality assessments and the concept of double materiality within the CSRD. In short, rather than an avalanche of mandatory disclosures for all aspects of sustainability, the final ESRS utilize a materiality assessment requirement for the topical standards. Therefore, companies must now assess and report on matters considered material to these topical standards based on a double materiality assessment.

The double materiality principle accounts for both financial and impact materiality, where companies must evaluate the financial risks and opportunities associated with sustainability matters as well as the effects on people and the environment. At a high level:

- Financial materiality focuses on how sustainability matters impact a company's business development, performance, and position

- Impact materiality focuses on just that – the impact a company has on sustainability matters, including environmental, social, and employee matters, along with respect for human rights, anti-corruption and bribery matters, and governance

Most importantly, information on sustainability meets the double materiality criteria if it's material from the impact perspective, financial perspective or both. In practice, that means businesses must consider the two materiality perspectives individually. From there, they must disclose information needed to understand how sustainability matters affect them, as well as information necessary to understand the impact they have on people and the environment.

ESRS Changes from the Draft Standards

Moving on, we also want to touch on a few crucial areas where the final standards vary pretty considerably from the November 2022 draft ESRS standards. All modifications by the EC were intended to provide relief to companies in their application.

Phasing-In of Reporting Requirements

Understanding that sustainability reporting requirements can pose significant challenges to companies – especially smaller ones – the ESRS include phase-in relief measures to help with the implementation of the new reporting processes.

For example, in the first year of applying the new standards, companies with less than 750 employees may omit specific data points and disclosure requirements related to Scope 3 GHG emissions data as described in ESRS S1. Likewise, for the first two years, these smaller entities may also forgo disclosure requirements described in the standards on biodiversity as well as those on value-chain workers, affected communities, and consumers and end-users.

Further, the ESRS allows all reporting entities to omit anticipated financial impacts around non-climate environmental issues – pollution, biodiversity, water, and resource use – in the first year of application. Also, companies need only provide qualitative disclosures on the financial impacts of these disclosures for a further two years.

Additionally, in that first year, businesses can exclude certain data points related to their own workforce – again, those falling under the ESRS S1 standard – including those on persons with disabilities, work-related ill health, social protection, and work-life balance.

Voluntary and Mandatory Disclosures

To maximize flexibility and reduce potential reporting burdens, the final ESRS also include a number of voluntary disclosures. The list of previously mandatory disclosure requirements was removed – namely E1 and S1 – and is now subject to a company's materiality assessment like any of the other topical standards. Such voluntary disclosures include topics like biodiversity transition plans, indicators related to nonemployees in the workforce, and explanations on why particular sustainability topics are considered nonmaterial.

Flexibility in Particular Disclosures

Continuing the flexibility theme, the final standards provide options for disclosing financial impacts from sustainability risks, stakeholder engagement, and selecting a methodology for the materiality assessment process. In doing so, the ESRS allows organizations to build their sustainability reporting processes to best suit their specific circumstances, all without sacrificing the integrity and transparency of the sustainability disclosures.

Interoperability with Other Standards

Obviously, the ESRS don't exist in a bubble. Between the many existing frameworks and different regulators – including the SEC – developing and refining their own ESG reporting requirements, the EC and EFRAG have made a concerted effort to increase interoperability between standards.

This is a particular concern for multinational companies since they may be subject to rules, standards, or frameworks across many jurisdictions. Thankfully, the EC has spoken about ensuring a high level of alignment between the ESRS, the ISSB standards, and the Global Reporting Initiative (GRI).

In fact, the EFRAG and ISSB developed their separate sets of standards – the EFRAG's ESRS and IFRS 1 and 2 from the ISSB – in parallel with each other. Therefore, companies compliant with ESRS on climate change will overwhelmingly be compliant under the ISSB standards as well.

That doesn't mean, however, that companies should assume compliance with other standards just because they meet those of one. This is particularly true for the ever-gestating climate disclosure rules of the SEC, where several critical differences exist with respect to the ESRS:

- Scope – The SEC is exclusively climate-focused and industry-agnostic while the ESRS requires full sustainability disclosures, including industry-specific ones

- Materiality – The SEC only includes financial materiality with a focus on investors whereas the ESRS uses the double materiality concept

Next Steps

Now that we know what the CSRD and ESRS have in store for companies in the not-so-distant future, businesses need to get their sustainability reporting houses in order. And fast. But where do you go from here? Well, our comprehensive guide on ESG reporting is an excellent place to start, providing an expansive look at everything you'll need from your people, processes, and technologies for efficient, effective sustainability reporting. To get you started on the ESRS, however, we have a few different areas for you to hone in on.

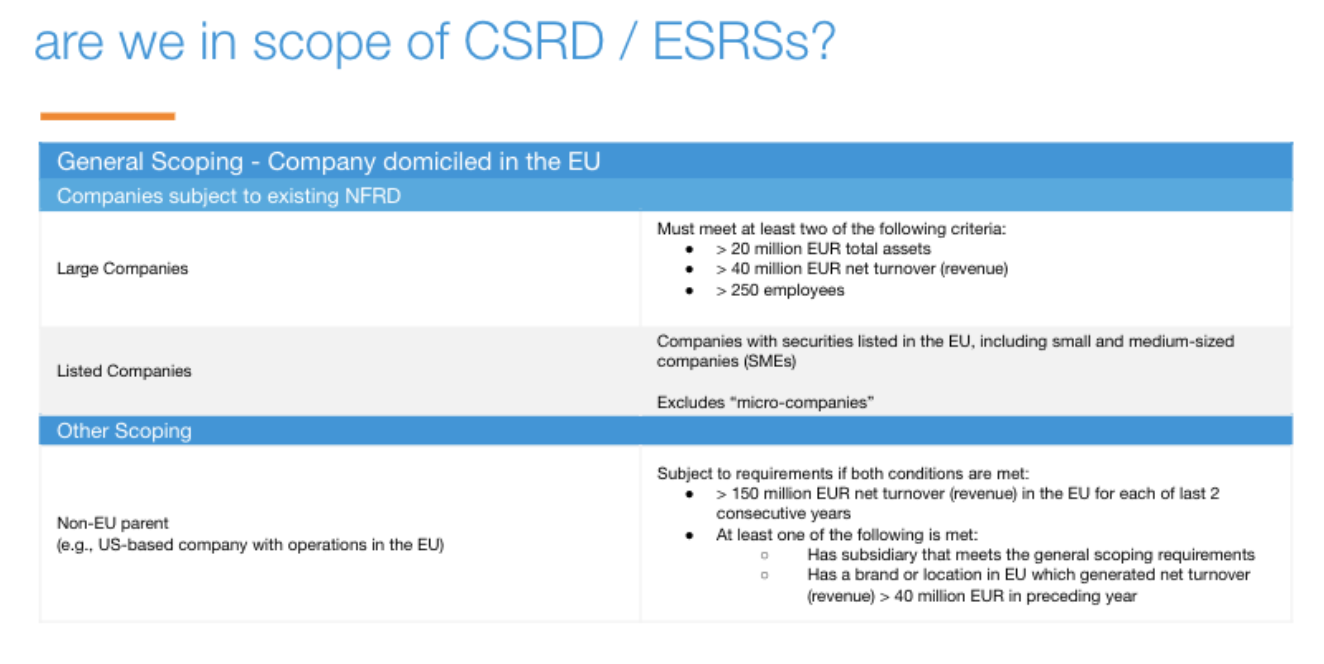

Scoping Provisions

Remember, the CSRD isn’t exclusive to EU-based organizations. To that point, early research estimates more than 10,000 non-EU companies – 3,200 from America alone – will fall within the CSRD's grasp.

As you can see from the graphic, there’s plenty of room for non-EU companies to fall in scope of the CSRD and its ESRS. To make things even easier for our US parent company friends, we’ve also created a handy scoping decision tree:

Whether you're in scope for the CSRD or not, though, sustainability reporting and strategy will impact you in some way, even if you're a private company. Remember, just because you don't have the legal or regulatory obligation to adhere to the ESRS, IFRS, or any other sustainability standards, those around you will still expect them, from investors and lenders to value chain partners and more. Therefore, like it or not, sustainability reporting will inevitably be a part of your future. No ifs, ands, or buts about it.

Materiality Assessment and Related Tasks

Of course, the double materiality assessment is front and center in the ESRS standards, making it an obvious focal point for you. From a practical perspective, the assessment involves determining and ranking your most impactful sustainability opportunities and risks, as determined by market data, stakeholder interviews, and surveys. And all of that is going to take some time and effort.

Once again, this is especially true for multinationals since they have so many moving parts within their operations. Thus, to start assessing the impact of the CSRD and ESRS, organizations should:

- Review entity structure to determine in scope companies or undertakings like, for example, reporting boundary assessments

- Consider reporting options and strategies to meet requirement timelines

- Perform double materiality assessments

- Review ESRS and begin implementing processes necessary to comply with the requirements, including a reporting and disclosure gap assessment, review of current control environment, and remediation of the findings

Sustainability Data Systems and Processes

You'll need accurate data to report on sustainability and ESG performance. But what data should you focus on in the first place? As you might've guessed, the materiality process will shed a powerful light in that regard, revealing sustainability themes you should target for data collection, analysis, and reporting.

Remember, this data can come from a broad spectrum of your operations, depending on what components of them account for your company's carbon footprint. Therefore, from business travel to manufacturing lines, you're on a hunt for relevant data, whether that's sitting in spreadsheets, a spiderweb of repositories, or somewhere else.

The bottom line is this – there's a lot to do and not a ton of time to do it, as yet another helpful graphic demonstrates.

.png?width=667&height=375&name=image%20(22).png)

And as if you needed an even greater sense of urgency, these initial ESRS are only the beginning. Down the road, the EFRAG will be developing and releasing additional standards, including sector-specific ESRS, simplified ESRS for small-medium sized entities (SMEs), and non-EU parent-specific ESRS.

Now, with any luck, you’ll have the in-house experience and expertise to get everything done and ensure you're not in a mad scramble as effective dates get closer and closer. However, most organizations don't have that luxury, making specialists like Embark invaluable as you look into the ESG-tinged future. From your processes to systems and everything in between, our ESG and Sustainability team is ready to transform your reporting into a distinct advantage that sets you apart. So let's talk.