|

In this article |

The information environment has changed

Finance and accounting teams have always understood that the information they produce has two lives: an internal one, in which it informs management decision-making, and an external one, in which it communicates the company's financial condition to investors, lenders, auditors, and other stakeholders. The discipline of financial reporting is fundamentally about the integrity of that translation — ensuring that what leaves the finance function accurately represents what happened inside the business.

That external life is now more complicated. Large language models and AI-enabled analytical tools are increasingly part of how sophisticated investors, analysts, and counterparties process and interpret financial disclosures. These tools don't read the way humans do. They ingest, extract, classify, and compare at scale — across quarters, across peers, across the full body of a company's public filings simultaneously. And when they encounter information that is ambiguous, inconsistently labeled, or structured around internal conventions that don't translate cleanly to external consumption, they produce outputs that can misrepresent what the finance team worked hard to communicate accurately.

This isn't primarily an investor relations problem. The quality, consistency, and structure of the underlying accounting and financial data determines whether AI-assisted analysis of that data is accurate. Finance and accounting teams sit at the origin point of that quality — which is exactly why this shift in the information environment matters to them directly.

AI in the drafting workflow

At the same time that AI tools are changing how external audiences consume financial information, they're also changing how finance teams produce it. Generative AI is increasingly present in the disclosure drafting process — from earnings press releases and earnings call scripts to risk factor language and MD&A sections. Research published in the Journal of Accounting Research in 2026 examined actual filings through 2024 and found statistically significant generative AI usage across earnings press releases, conference call prepared remarks, risk factors, MD&As, and IPO.

For finance teams managing high-volume, time-pressured reporting cycles, AI drafting tools offer real efficiency benefits: faster first drafts, automated cross-period comparisons, and the ability to surface language from prior filings at scale. The productivity case is legitimate.

But AI-generated disclosure language introduces risks that sit squarely with the finance and accounting function, not just the team that presses publish. The accuracy of an AI-generated revenue recognition disclosure depends on whether the underlying accounting judgment was clearly documented in the first place. The accuracy of an AI-generated MD&A depends on whether the finance team's analysis was specific and structured enough for a model to interpret correctly. Garbage in, garbage out applies here — and the garbage, if it exists, originated upstream of the drafting step.

|

Embark insight

AI drafting tools are a first draft, not a final one. The finance team owns the output — including the accounting accuracy of what AI produces from its inputs. Workflow governance around AI-assisted drafting isn't a technology question; it's an internal control question. |

What happens when your data reaches an AI-assisted reader

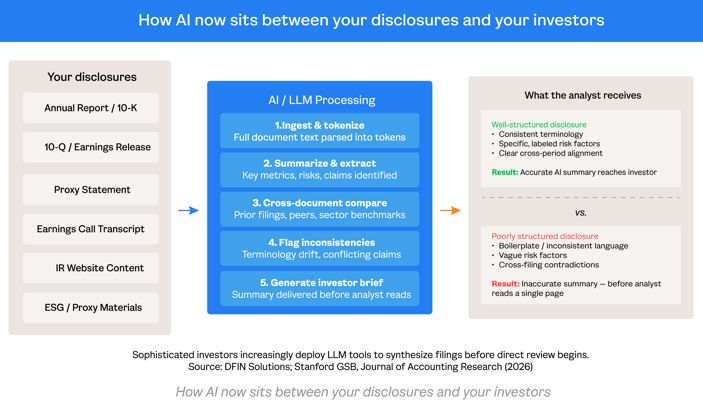

Understanding the practical mechanics is useful context. When an analyst's AI tool processes a company's 10-K, it doesn't read the document the way a human analyst would — building a mental model of the business over time and filling in gaps with context. It tokenizes the text, extracts defined concepts and labeled quantities, and compares them against prior filings and peer company disclosures using pattern recognition rather than interpretive judgment.

That process is highly sensitive to consistency and structure. Terminological drift — using "gross profit" in one filing and "gross margin contribution" in another to describe the same line — doesn't just create a readability problem. It creates an extraction failure. An AI tool comparing the two filings may classify them as describing different metrics and produce a comparison that overstates change or flags a discrepancy that doesn't exist.

Similar dynamics apply to segment reporting changes, reclassifications, non-GAAP measure redefinitions, and changes in the presentation of key performance indicators. When these changes are clearly explained in the filing — which GAAP already requires in most cases — AI-assisted readers process them correctly. When the explanation is buried, absent, or written in language that's ambiguous to pattern-matching systems, the outputs degrade.

The practical implication is straightforward: the accounting precision and disclosure rigor that good financial reporting practice has always demanded is now doubly important, because the audience for that rigor includes both human readers and the AI tools those readers rely on.

The accounting disciplines that matter most

Reexamining a few specific areas of accounting and disclosure practice through this lens is worthwhile:

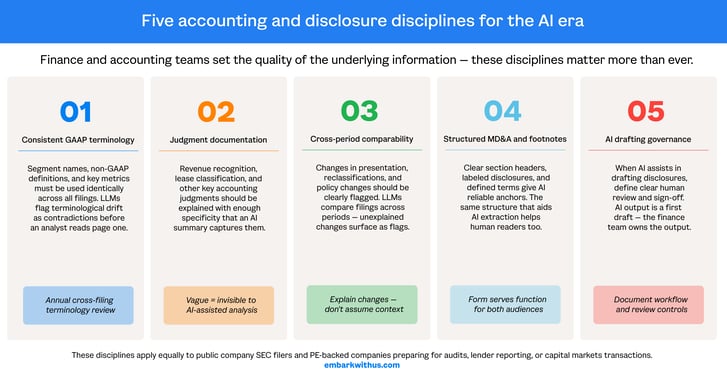

Non-GAAP measures. Non-GAAP measures are among the most frequently queried elements of financial disclosures, and they're also among the most likely to drift in definition across periods or to be labeled inconsistently between the earnings release and the 10-K or 10-Q. Finance teams that allow non-GAAP definitions to evolve without explicit disclosure of the change are creating extraction failures for AI tools and, separately, potential SEC comment exposure. Clear, consistent, period-over-period comparability in non-GAAP presentation is a disclosure quality issue that predates AI — but AI makes its absence more consequential.

Revenue recognition disclosures. The level of specificity in revenue recognition disclosures under ASC 606 varies considerably across companies and industries. Disclosures that describe performance obligations, variable consideration, and contract asset movements in general terms may satisfy the technical requirements of the standard while providing insufficient signal for AI-assisted analysis to extract meaningful, comparable information. Finance teams should consider whether their revenue recognition note is specific enough to be interpretable without the surrounding context a human analyst would bring.

Segment reporting. Segment changes — disaggregations, reaggregations, or realignments of how management views the business — require careful disclosure under ASC 280, and they're exactly the kind of structural change that creates cross-period comparison errors in AI-assisted analysis. When segment structure changes, the explanation of what changed and why, along with recast prior-period comparatives where provided, is critical to ensuring that automated comparisons don't produce misleading conclusions.

Critical accounting estimates. Disclosures about critical accounting estimates are a primary target for AI-assisted extraction by analysts assessing earnings quality and the sustainability of reported results. Generic, boilerplate language in this section — describing estimates as "significant" without explaining the magnitude of potential variability or the key assumptions driving them — is both a disclosure quality weakness and an AI extraction failure. Specific, quantified critical accounting estimate disclosures are more useful to investors and more accurately processed by AI tools.

Governance: finance team ownership of AI-assisted workflows

The governance question follows directly from the workflow question. If AI tools are involved in drafting any part of your external financial disclosures — and for a growing number of finance teams, they are — the finance function needs a clear answer to a few foundational questions.

Who reviews AI-generated draft language before it's incorporated into an external document? The review responsibility should sit with someone who has the accounting knowledge to evaluate the accuracy of the output, not just the editorial judgment to assess whether it reads well. An AI-generated description of a revenue recognition policy change needs to be reviewed by someone who understands the accounting, not just someone who can identify awkward sentences.

How is accuracy verified against the source? AI language models can produce plausible-sounding financial disclosure language that is subtly inaccurate — numbers transposed, periods conflated, conditions omitted. The verification step needs to be explicit: AI-generated draft language should be traced back to the underlying accounting records and documentation before it is finalized.

Is this documented in your control framework? For public companies, this question connects directly to ICFR. The CEO and CFO certifications required under Sarbanes-Oxley attest to the effectiveness of internal controls over financial reporting — and those certifications attach to the final disclosure regardless of what tools produced a draft. If AI is in your drafting workflow and that workflow isn't documented and controlled, the certification carries a gap that auditors and regulators are increasingly equipped to find.

| For PE-backed companies: The accountability framework is different, but the underlying discipline is the same. Audit readiness, lender covenant compliance, and preparation for a future capital markets event all require that management's financial representations are accurate, traceable, and supported by adequate review. The absence of a SOX certification doesn't reduce the accountability; it just changes who's asking the question. |

These aren't new internal control principles. They're existing ICFR disciplines extended into a workflow that didn't exist five years ago. The question most finance teams haven't yet answered is whether their existing control environment covers the new ground.

A rising floor for disclosure quality

None of this changes the fundamentals of what good financial reporting looks like. Completeness, accuracy, consistency, specificity, and clarity have always been the standard. What's changed is the consequence of falling short of that standard.

When the primary audience for financial disclosures was human analysts working through documents manually, disclosure quality that was adequate but not excellent could be partially compensated for by context, by relationship, by the analyst's own knowledge of the company's history. AI-assisted analysis doesn't compensate. It extracts what's there and flags what's missing or inconsistent, and it does so at a speed and scale that means those flags can reach investors before the finance team has a chance to contextualize them.

The finance and accounting function has always been the guardian of the integrity of financial information. That role hasn't changed — but the environment in which it operates has. The AI tools that investors are using to analyze financial disclosures are, in a real sense, a stress test of disclosure quality that runs continuously and at scale. Finance teams that treat this as a reason to raise their own standard will find it a competitive advantage. Those that don't will find the gap exposed in ways that are harder to manage.