|

Update – April 2025: While this marks a significant shift at the federal level at this time, climate-related disclosure requirements continue to gain traction at the state and international levels. Public companies may still face reporting obligations under laws like California’s SB 253 and SB 261 (as amended by SB 219), the EU’s Corporate Sustainability Reporting Directive (CSRD), and other frameworks aligned with the International Sustainability Standards Board (ISSB). We encourage companies to stay current on these evolving requirements and continue preparing for compliance where applicable. |

Finally. After nearly two years of hemming and hawing, the Securities and Exchange Commission (SEC) has released its groundbreaking rule on climate-related disclosures. The decision is expansive, with the final rule encompassing over 800 pages of small-font print, and represents a significant shift in the regulatory landscape. Now, by enforcing environmental transparency on how climate risks impact registrants and accountability over their reporting, the disclosure rules give investors critical and comparable information they need to make informed decisions. And that’s great.

However, for corporate finance leaders—especially those waiting for the final ruling—the journey is just beginning. Since the final ruling introduces some notable adjustments from the initial proposal, companies must now set a new course on navigating their disclosure requirements. And that’s exactly what we’re discussing today.

Background on the New SEC Climate Disclosure Rule

To say the least, this final climate-related disclosure rule has taken a long and winding road to the Federal Register promised land. It’s been two years, in fact, with several starts, stops, and detours along the way. In many ways, the drawn-out process reflects the complexity of creating such a comprehensive regulatory framework, one designed to give investors the transparency they expect into climate issues.

Ultimately, the ruling is the product of seriously meticulous consideration and input from a broad range of stakeholders. Although its 886-page body is sprawling and often tedious, its heart aims to provide a robust and genuinely forward-thinking policy that aligns with the growing investor demand for, once again, transparent and meaningful climate risk information.

A Close, Contentious Vote

That’s not to say, however, that the sprint to the finish line lacked drama. In a closely watched decision, the SEC voted 3-2 in favor of adopting the final rule, shining a bright spotlight on many of the concerns that keep ESG such a hot-button issue. In particular, this outcome:

- Highlights the never-ending, contentious nature of the debate surrounding climate disclosures, not to mention climate change as a whole;

- Marks a significant step in regulatory efforts to weave environmental considerations into corporate reporting;

- Reflects a broader dialogue on climate change and the role of corporations in addressing environmental challenges.

Agree or disagree with the SEC’s approach or climate reporting in general, there’s no denying that the finalization of this climate disclosure rule represents a pivotal development in the relationship between regulation, corporate accountability, and investor expectations.

Key Aspects of the SEC's Final Climate Disclosure Rule

Zooming in on the actual rule, the announcement has elicited a range of initial reactions, from excitement to a keen sense of the challenges ahead. Of course, this just underscores the rule's significant impact on disclosure practices and how companies must adapt.

After our team’s first read-through of the rule, we walked away with three immediate, high-level takeaways:

- Expansion of Disclosure Requirements: The rule extends beyond traditional financial disclosures and targets detailed climate-related information. This expanded reach speaks to the growing demand from investors for a more comprehensive view of a company's environmental impact and climate risk exposures.

- A Shift in Investor Priorities: Such detailed climate risk information in financial disclosures also indicates a broader shift in the investment community. To reiterate, investors are factoring environmental considerations into their decision-making processes to a far greater degree now, driving the need for more transparent, comparable, and relevant disclosures.

- Far-Reaching Implications for Companies: From a practical perspective, the rule means businesses must reevaluate their reporting processes, including adopting more rigorous data collection and analysis practices as well as establishing appropriate controls to comply.

Scope 3 Emissions: A Major Exclusion in the SEC's Final Climate Disclosure Rule

Besides our initial takeaways, several adjustments from the proposed rule also stood out. While we’ll take a closer look at most of those changes in the near future, we wanted to focus on one particular change with this initial reaction – the Scope 3 emissions exclusion.

Understanding the Scope 3 Exclusion

As we said in some previous insights on ESG reporting, Scope 3 emissions are indirect emissions occurring throughout the value chain, from sourcing raw materials and waste generated to delivering the final product. Needless to say, this topic has been a focal point for public feedback, industry concerns, and general discourse, likely responsible for much of the ruling’s perpetual delays.

Of course, excluding Scope 3 emissions from the final ruling won’t necessarily stop the topic from being such a point of discussion, especially since they’re still very much a part of the EU’s European Sustainability Reporting Standards (ESRS) and new climate reporting laws in California. Further, while some stakeholders will view the exclusion as a pragmatic approach to admittedly steep Scope 3 reporting challenges, others will undoubtedly see it as a missed opportunity to fully account for a company's climate impact.

But we’re not here to opine on the merits or feasibility of Scope 3 emissions reporting. Instead, we’re just reporting the facts. And in this instance, those facts speak to the extremely complex nature of Scope 3 emissions. Suffice it to say, concerns about the difficulty in accurately measuring and reporting these types of emissions played a massive role in their ultimate exclusion.

The Future of Scope 3 Emissions Reporting

All that said, as the SEC continues to navigate the topsy-turvy, ever-changing landscape of climate risk reporting, the dialogue behind Scope 3 will undoubtedly continue, even though they’re not part of the SEC’s climate disclosure rule, at least for now. Remember, because of other U.S. state laws and global regulations, companies may still need to consider the broader implications of their value chain emissions at some point, even if the SEC doesn’t currently require it.

Surprises and Highlights in the SEC's Final Climate Disclosure Rule

Before rounding things out with a few last-minute insights, we’d like to reiterate that what we’ve discussed today is just the tip of the proverbial iceberg. So, while these initial thoughts are useful in familiarizing yourself with recent events, they’re in no way comprehensive—not even close. To that point, we’ll follow up with a much more thorough look at the SEC rules and, most importantly, what they might mean for you and your reporting. For now, however, we want to round things out with a few areas that caught our eye in the final rule.

1% Threshold for Certain Expenditures

One of the biggest surprises was the relatively low—1%—materiality threshold for certain expenditures related to climate-related risks. Granted, this requirement is quite different—and less onerous—from what was included in the proposed rule, and the SEC did also include de minimis thresholds here. Still, however, this really speaks to the SEC's genuine effort to give investors access to a broad set of information, even when the financial impact might be marginal by traditional standards.

Scope 1 and Scope 2 with Materiality Consideration

The rule also mandates the disclosure of Scope 1 direct emissions from owned or controlled sources as well as Scope 2 indirect emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the reporting company. Unlike Scope 3, the SEC obviously determined the practicalities of data collection and reporting for Scope 1 and Scope 2 emissions were both feasible and warranted, given investor demand for transparency.

Specifically, the added emphasis on materiality stood out to us in this area of the GHG emissions reporting requirement. In short, the rule mandates that disclosures for Scope 1 and Scope 2 emissions must consider whether the information is material to investors, introducing a layer of judgment to the GHG emissions reporting process. This consideration is pivotal in ensuring company disclosures are both relevant and useful to investment decision-making.

Timeline Adjustments in the SEC's Final Climate Disclosure Rule

Closing out our initial reactions, the SEC's final climate disclosure rule also introduced significant changes to reporting timelines and assurance requirements.

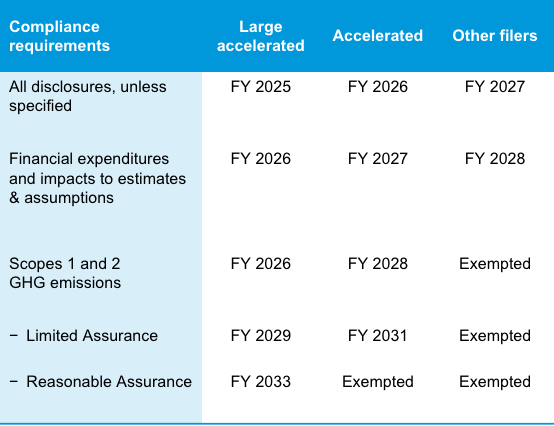

- Large Accelerated Filers: Most of the disclosures under Regulation S-X and Regulation S-K will be required starting in 2025. Some disclosures will be phased in during 2026, including the GHG report, which also has a phased-in timeline for assurance levels.

- Accelerated Filers: A similar timeline to large accelerated filers applies, with the main difference being an extra year to comply with certain requirements. The GHG report deadline for this group extends to 2028.

- All Other Filers: These entities have an additional year beyond the deadlines set for accelerated filers.

Assurance Requirements: Phased Introduction Over Time

The SEC's final rule also outlines a phased approach to assurance for GHG emissions reporting:

- Large Accelerated Filers: The rule requires limited assurance in fiscal year beginning 2029, focusing on verifying the reliability of the GHG emissions data reported. Reasonable assurance is required in fiscal year beginning 2033.

- Accelerated Filers: The rule requires limited assurance in fiscal year beginning 2031, again focusing on verifying the reliability of the GHG emissions data reported. The rule doesn’t establish a timeline for reasonable assurance requirements.

We’ve also collected the timeline and assurance requirements in a handy dandy table for you:

Going Forward: Where Do You Begin with the Final SEC Climate Rule?

Given the sheer size and scope of the final rule, we’ll be going into far greater detail shortly down the road. With these initial thoughts, however, we wanted to help you take a baby step on the path to compliance. So, that said, besides beginning to absorb what the new rule entails, where do you go from here? Well, off the top of our head:

- Assess your Readiness and Enhance Reporting Processes: Spend some quality time evaluating your current reporting abilities, identifying any gaps, and building the necessary infrastructure to meet the expanded requirements.

- Develop a Strategic Approach to GHG Emissions Reporting: With Scope 1 and Scope 2 emissions in the spotlight, you need to prioritize accurate data collection and analysis, considering both direct and certain indirect emission sources.

Sure, there’s an awful lot more to effective, efficient sustainability reporting than just getting a lay of the data and reporting land, but you have to walk before you run. Therefore, our advice is to pore over our comprehensive guide, ESG Reporting Best Practices: Implementation & Beyond, to fully understand the critical steps you need to take to get and stay compliant with any sustainability reporting standards that may come your way, whether from the SEC, EFRAG, or anyone else.

Of course, you still have a business to operate in the meantime, and your team already has a full plate of everyday responsibilities. But that’s what makes Embark’s ESG and Sustainability team such an ace-in-the-hole for you. We have the knowledge, skills, experience, and bandwidth to help you start addressing your ESG reporting today. As in, immediately. So, assuming you don’t want to get on the wrong side of the SEC and its spiffy new climate-related disclosure rules, let’s talk and see what we can do to get you compliant. Because the regulatory clock is ticking.